What is the FX Carry Trade?

A carry trade is a trading strategy at the core of active currency management. It sees an investor borrow capital in a currency that has a low interest environment, such as Japan (0.75%), and invest the borrowed funds into a currency where there is a high interest rate, such as Mexico, Brazil, and Egypt (7%, 15%, and 20% relatively). These latter target currencies offer a higher yield, and this can be denoted as a ‘risk-on environment’. This strategy intends to gain profit from the ex-ante positive interest rate differential.

This strategy, by logic, seems an effortless and remunerative route to achieve simple profit. In reality, this carry trade faces more predicaments, one of which is the theory onUncovered Interest Rate Parity (UIP). Since anFX carry trade is usually conducted using forwards (although futures and swaps can also be used). The UIP theory states that this carry profit is harder to achieve because when forward products are used, the forward exchange rate is meant to be higher to reflect the spot rate, and close out this interest rate differential gap. If UIP theory holds up the expected return should end up being zero.

Nonetheless, the FX carry trade is still postulated here as a possible strategy, due to the frequent failure of UIP to materialise, which is coined the ‘carry trade puzzle’. This is where currencies with high interest rates, tend to appreciate more – going against UIP, (which proposes these currencies should theoretically depreciate). Thus, the subsequent buying pressure on the quote currency enables it to appreciate even more, this enables the trade to be existentially embedded.

An article from 2014, by Daneil, Hodrick and Lu, advances that the time-varying dollar exposure of the carry trade is at the core of the carry trade puzzle. The US dollar matters to carry trades, even when both the base currency and quote currency are not USD. Carry trades are not just bilateral transactions; they are relative, and load on a global risk factor – the US dollar.

Yet, this sensitivity is not constant, the beta of the carry returns changes over time. When a carry trade expects high returns in a risk-on environment the dollar exposure can seem small or negative. In the parallel situation, in a risk-off environment, the dollar strengthens, investors unwind carry positions, and dollar exposure will then grow and be positive, which is when returns will be the worst for carry trade positions. This can help explain why the carry trade puzzle occurs. In essence, UIP theory accounts for constant risk and does not encompass the dollar’s tie to non-dollar carry trades, and that the dollar’s risk is nonlinear.

Going beyond this, high interest rate currencies, for example the Turkish lira and Egyptian pound, tend to trade at forward discounts (a currencies forward rate is lower than its spot rate), relative to the low interest rates currencies. In comparison to low interest rate currencies, which trade at forward discounts (the currencies forward rate is higher than its spot rate). Accordingly, the carry trade still suffices by carrying out a long position in forward markets where forward discounts are present. On the parallel side, the carry trade can still be implemented when going short in currencies where a forward premium is present.

Additionally, this trading strategy comes with another significant risk. Countries with a high interest rate, are usually positioned against highly volatile markets tied to a fickle geopolitical landscape. Unwinding of risky positions can happen when volatility takes form. As such, carry trades work best in quiet markets.

The discussion on the risk premium on a FX carry trade is further nuanced than this and can be divulged more by looking at market variance. Market variance in FX, involves measuring how much an exchange rate deviates from the average mean trend over a time period. Higher variance measure means there are larger, jumpier, and more unpredictable moves from the average. A low variance measure, indicates smaller, steadier and more predictable moves from the average. Market variance is the average of the squared deviations from the mean return. On a futile level, market variance is the sum of average variance + average correlation. Average variance can be broken down into how volatile, currencies are on average, while the average correlation shows much currencies move together.

A research article from Cenedese, Sarno, and Tsiakas (2014) explores on how market variance has a predictive power for indicating carry trade returns. This quoted ‘predictive power’, is primarily dependent on average variance, which also has a noticeable negative effect on the left tail of future carry trade returns. Moreover, the trustworthiness of market variance as a predictability tool of carry trade returns is shown to be more reliable in crucial periods.

FX Carry Trade Suggestions: CHF/COP and USD/TRY

CHF/COP

- Swiss Rate Hold

Many central banks in 2026 are seeing this year as an end to their rate-cutting cycle, evident by The Fed’s rate hold on January 28th, followed by previous cuts in 2025. The Swiss National Bank has the same sentiment of holding rates for the foreseeable future into 2026 at 0%, effective since June 2025. The Swiss central bank, appears to have no desire to increase rates, due to their low inflation, hovering year-on-year at around 0.0% to 0.1%, which is well below their aim. Therefore, CHF serves as an ample base currency here.

- The Dollar Connection

As uncovered previously, the dollar is tied to a carry trade even if not it is not involved. CHF is a safe-haven currency similar to USD, and due to a weakening dollar, other alike safe-haven currencies see demand fall. This creates an advantageous ‘risk-on’ environment, capital is encouraged to flow into high-yield currencies, in search for yield elsewhere, which puts a CHF/COP carry trade in good standing. If the dollar were to see a reversal and begin to strengthen, this could be a potential risk, as capital could be diverted into safer currencies once more.

- Colombia’s Monetary Policy

News coming out on January Friday 30th, reports how Columbia’s central bank has raised its base rate to 10.25%. This is an impactful contractionary policy movement, as this 100bp rise, is the first-rate hike in the past 3 years. This comes out following the report that core inflation of the nation picked up in December 2025 to 5.1%, with their aim of 3%. This attempt to inhibit prices, comes after an increase of 23.7% to the country’s minimum wage by Colombia’s president in December 2025.

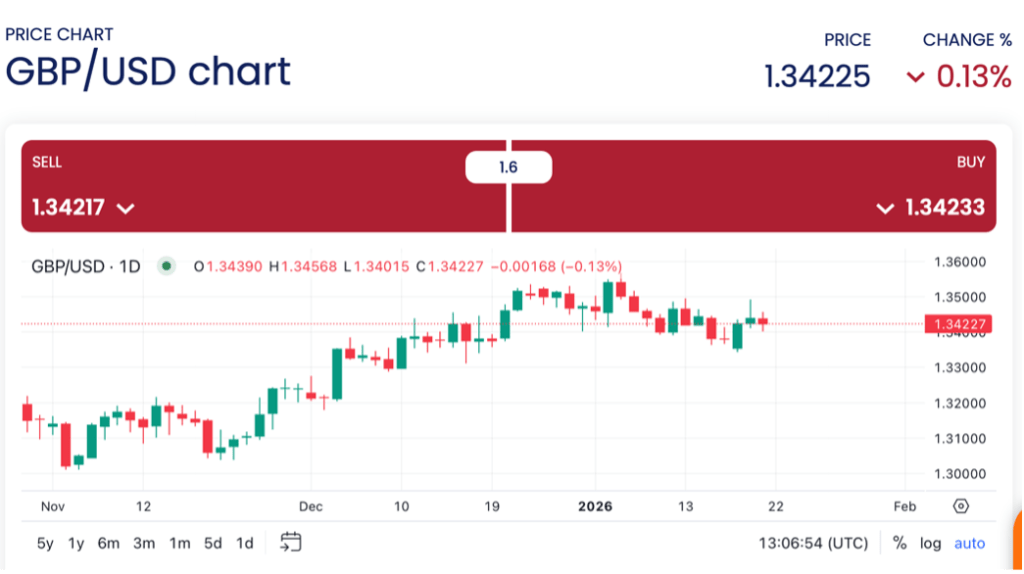

EM currencies have, according to the FT ‘made a roaring start’ in 2026, with Turkey, Brazil, Chile, Mexico, and others gaining 10% in dollar terms in January of this year. Colombia and Korea have performed the best with 20% gain in dollar terms. This is in part due to the weakening dollar, and also surged on with EM stocks outperforming other indices respectively, the US with the S&P 500, and the MSCI World seen below.

The risk premium on CHF/COP, is the geopolitical state of Colombia. This is in lieu of the backdrop of Venezuela and their tumultuous economic and political proceedings since January. Colombia has a forthcoming presidential election in May 2026; polls are unclear what the projections are, this will have to be watched closely in the run up to May. There is some positive outlook for Colombia, following the optimistic meeting between President Gustavo and President Trump on 3rd February, with the talk between the two deemed ‘constructive’. Their tricky relationship over the past year has been one damped by tensions around drug-trafficking in the Latin American nation, in which Trump denounced Gustavo was not doing enough, even turning a blind eye to the miss happenings. This positive feedback provides some assurance to investors regarding the stability of COP moving forward into 2026, despite an imminent election.

USD/TRY

For this second exotic currency pair suggestion – one with a somewhat lower risk premium is proposed. USD/TRY is an ample suggestion and a common FX carry trade, and more predictable than CHF/COP. USD is better served as the base currency over CHF in this instance, as USD/TRY is a much more liquid pair, and has lower transaction costs and faster execution, as CHF/TRY is traded much less.

As aforementioned, the Fed is contestably seeing the end of their rate-cutting cycle, after their most recent hold. Rates are forecasted to remain steady by JPMorgan this year between 3.5% to 3.75%, with one singular rate expected for 2026. On top of this, the value of the dollar as widely known, has fallen drastically in 2025, with the dollar index dropping nearly 10-11% by the year end of 2025. Last week, Tuesday 27th saw the dollar hit a four-year low. The weakness of the dollar is still expected to sustain, but at a less exponential rate as observed in 2025. Accordingly, the dollar seems a sufficient choice for a base currency in a carry trade.

- Turkish Monetary Policy

Turkey is also entering into a rate-cutting cycle, and has now cut 100bps from 38% in December 2025, to 37% in January 2026. Yet, this rate cut was 50bps lower than forecasted. The common consensus regarding Turkey’s central bank moving into 2026, is that rate cutting is expected to continue augmenting, and will be sitting at 27% by end of this year. The caveat to this projection comes out of Nomura, who advocate that their rate cuts will be less egregious, with predictions that TCMB will hold at their March meeting, with a year-end forecast of 29%.

Either route sees this interest rate differential still maintaining, and carry trade still able to be exploited, with short-dated forward rates (overnight to 1 month) closer to spot rates in the near term. The slight risk seen is in the long-term market (one year and above), where higher forwards rate starts to close out the interest rate differential gap, affirming UIP theory.

Lastly, in regard to the geopolitical state of the nation, and how this could influence the returns of this trade. Turkey sits at precious position both geographically and politically, as it is positioned at a sensitive crossroad between Europe and the Middle East. Risk-off events could spell sharp USD appreciation, against TRY, which could inhibit on returns. This will have to be watched carefully as we progress in 2026.

Disclaimer: Not financial advice