- The Defence Industry in 2026:

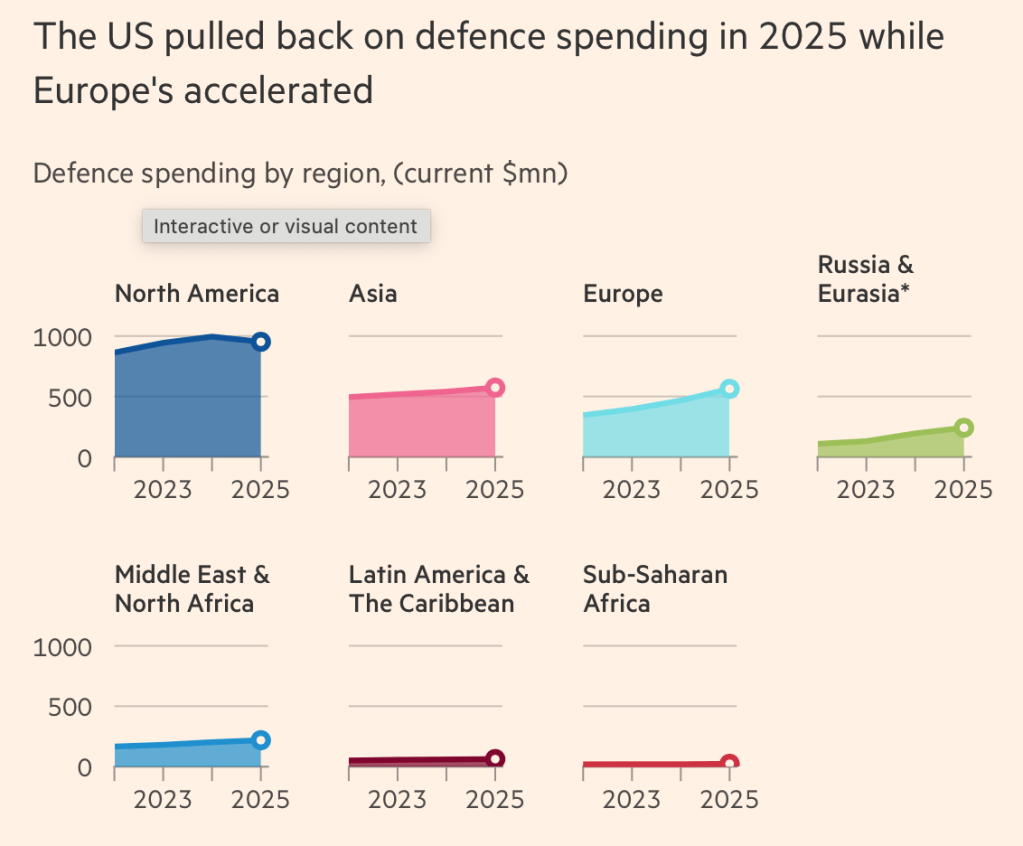

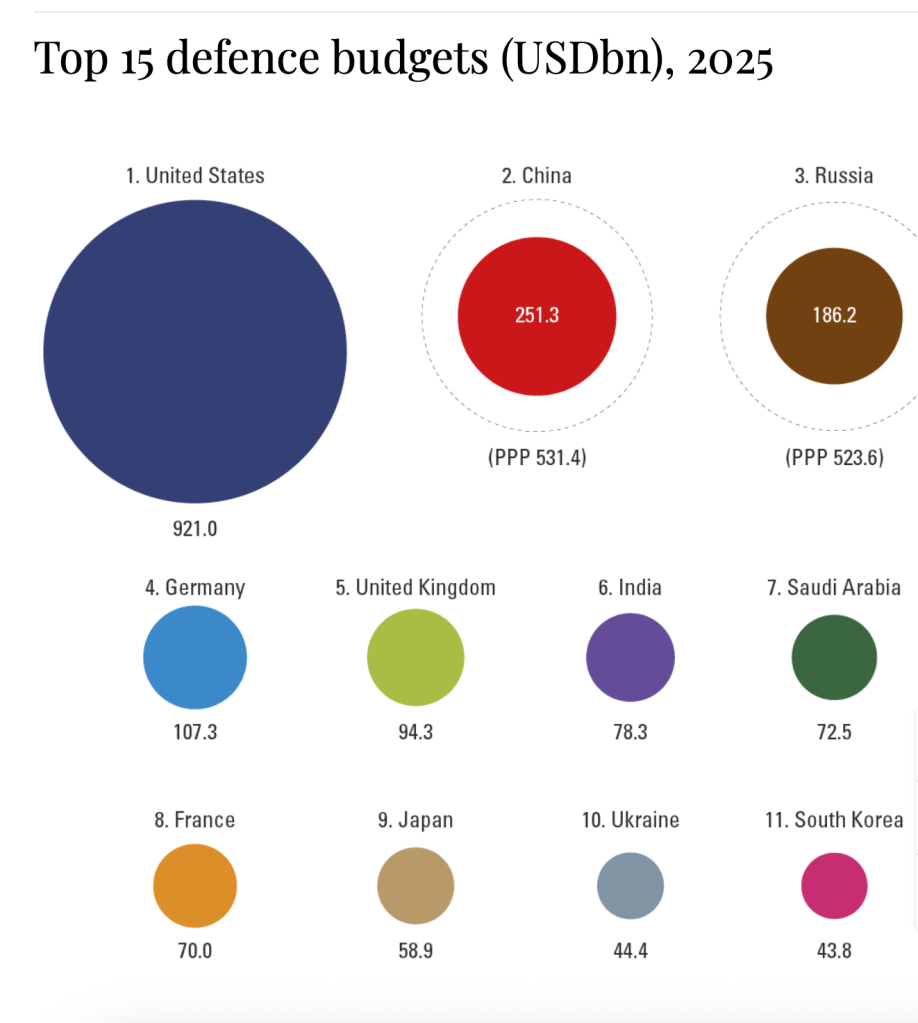

Washington has a track record of being the largest spender on defence globally, accounting to 36% of outlays in 2025. In 2025 the global defence spending was $2.63 trillion, a $15 billion increase from 2024. The FT reported yesterday that the IISS has provided data that the US defence expenses are easing down, but the EU is increasingly surging its bill, with Germany being the main bulk. Germany overtook the UK in 2024 as having the second largest defence budget in NATO, with the US still despite the relative slowdown, expenses 10 times more than the UK. Germany now accounts for 21% of the global total spending on defence, in comparison to 17% in 2022. Within the EU, France trails behind as the third largest spender on Defence, who had a $70bn budget in 2025.

The UK which is set to accelerate its spending from 2.5% of GDP to 3% under his tenure. The UK government in its 2025 Spending Review expected the MOD bill to come to £62.2 bn in 2025/2026, surging to £73.5 billion by 2028/2029.

The Council and European Parliament reached a provisional agreement on the EDIP (European Defence Industry Programme). The EDIP plans to provide €1.5 billion worth of grants from 2025 to 2027, in aid to enhance Europe’s defence industry.

Conversations at the beginning of this year around Venezuela, Greenland and Iran are set to spur a defence spending rally.

- Defence Composition Spending:

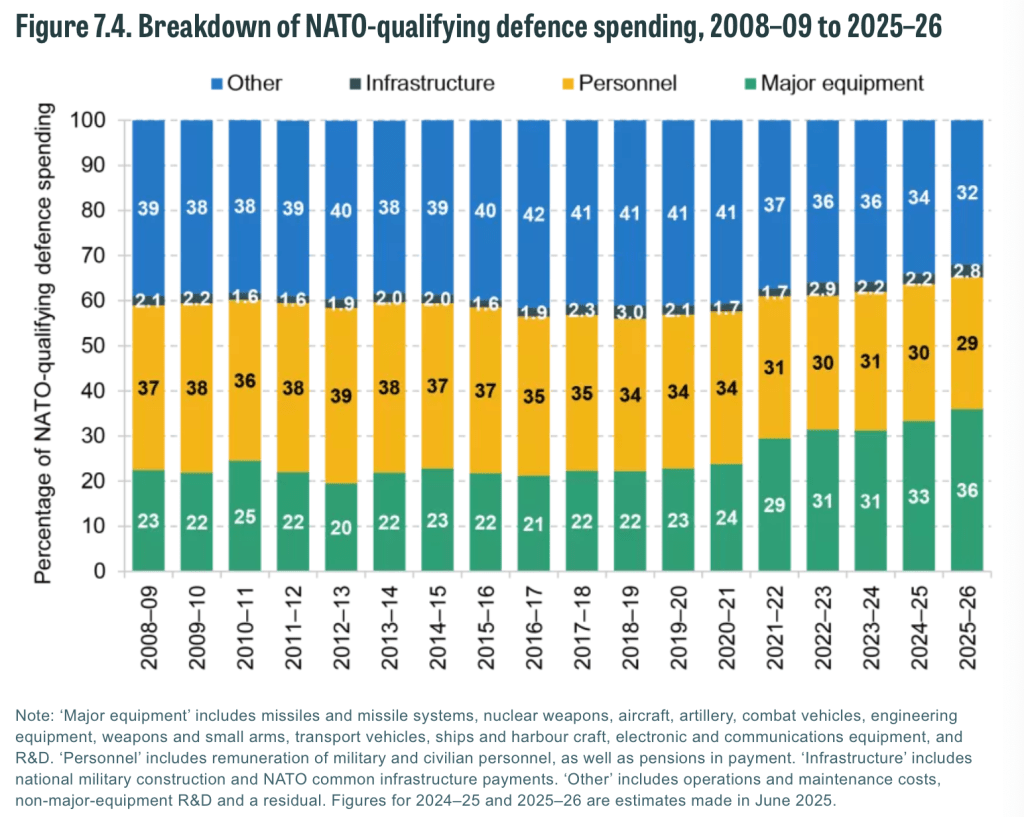

The composition of Defence spending in terms of where it’s going has augmented over time. Using data from the Institute for Fiscal Studies, breaking down NATO’s UK’s spending, major equipment is set to make up 36%, as of June 2025, aside from personnel and infrastructure, the remaining 32%, entitled ‘other’, includes costs covering R&D, non-major equipment, and operations. Major equipment is set to keep increasing, with shrinking personnel and infrastructure needs. The stock recommendations are reflective of these trends and supply needs expected.

A new avenue that can be capitalised on is the EU’s fresh commitment on space spending. Germany has the intention to spend $39billion and France $4.74billion by 2030 on space-based capabilities. The UK has further highlighted the necessity to divert funds to this opening by the nation’s Strategic Defence Review. Plus, NATOS’s Commercial Space strategy of 2025 advocated for loosened purse strings for what they term ‘commercially provided systems and services.’ The investment promotion is encouraged further by the EU defence representatives as the security of Europe wanes on US-provided space systems which Trump has autonomy over allocating to NATO. This renders this reliance unsustainable; the EU must build stronger space defence systems itself.

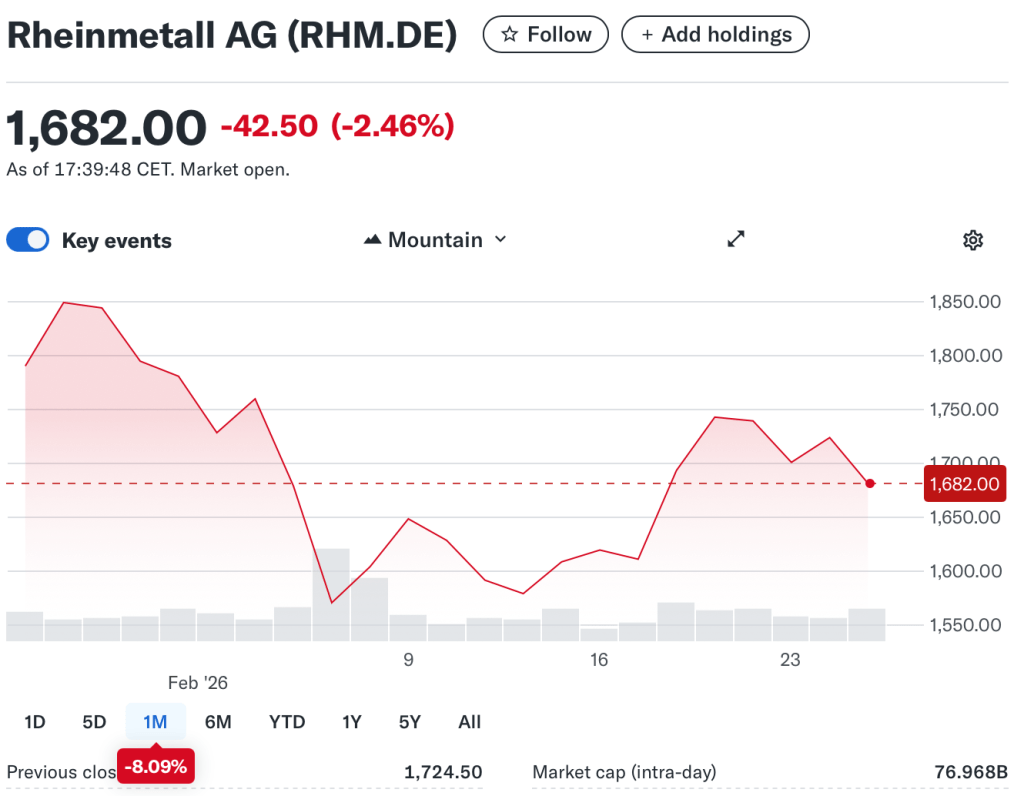

- Rheinmetall

News came yesterday that the Düsseldorf arms company, who construct tanks and ammunition, is set to be selected by Germany’s defence ministry as one of 3 companies to supply kamikaze drones. This contract will initially be worth €296mm and could be augment further if delivery deadlines of the products are met and performance needs are satisfied.

Morningstar believes some key European stocks are overvalued, such as Saab. Except Rheinmetall, they purport still has some upside potential. This is due to the stock previously staying solid during last year’s ongoing Ukraine conflict and discussions around NATO’s future. Morningstar denotes a 4-star rating to the company, compared to Saab with a 1-star rating and BAE Systems with a 3-star rating.

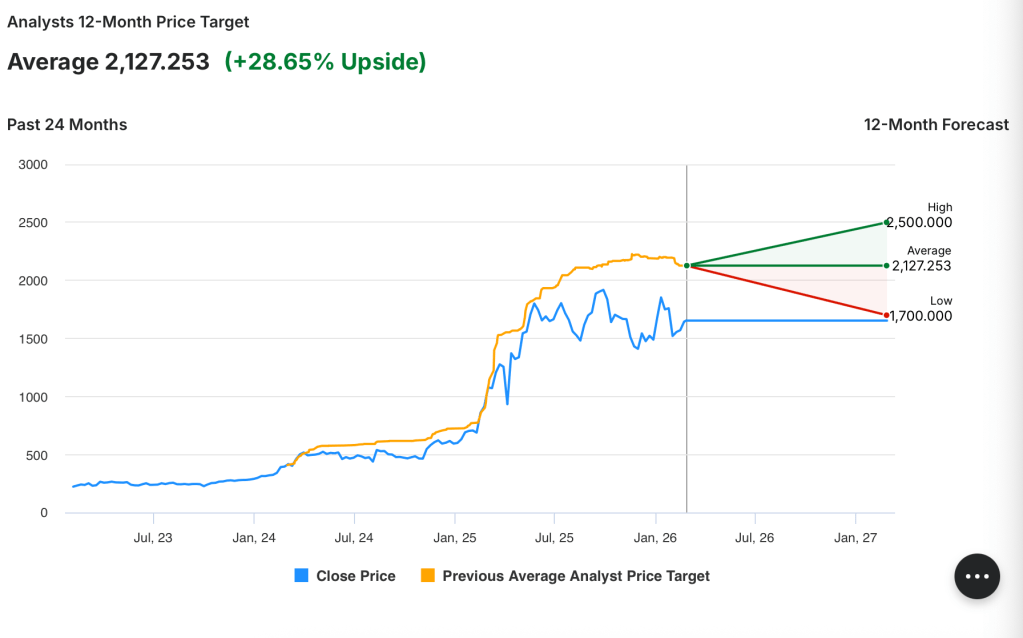

The company is viewed positively by analysts with the large majority advocating a buy, no sells observed and a small number of holds. Deutsche Bank advocating this status under the precedent set here of strong projected organic growth for company going past the 2030s. Barclays has the same under rationale of Germany as a core funding source. Berenberg is the same due to large order intakes from bolstered defence spending budgets, supporting cash-flow visibility. The Average 12-month price target for analysts sitting at 2,127.253.

In terms of risks, there are some valuation qualms; it trades a high forward P/E ratio of 42.55 well above its historical average, meaning much of the expected future growth may be already priced in. A downside of this to be aware of is the company must now deliver,; otherwise the P/E compresses and the stock falls hard. The beta (5-year monthly) is around 0.40, indicating the stock is substantially less volatile than the market, but this can be purely indicative of the defence sector having lower than usual betas due to defence the industry having a less cyclical disposition.

Other risks include the German Chancellor Friedrich Merz and the finance minister, stating that they have concerns that large manufacturers, of which Rheinmetall was named, will disproportionally benefit from their defence budget. They believed small highly specialised SME’s, which drive key innovations, should also receive adequate amounts in order to create ‘maximum spill over on the whole economy’, the FT reports. Overall, Rheinmetall appears a good long-term buy, but with some near-term volatility.

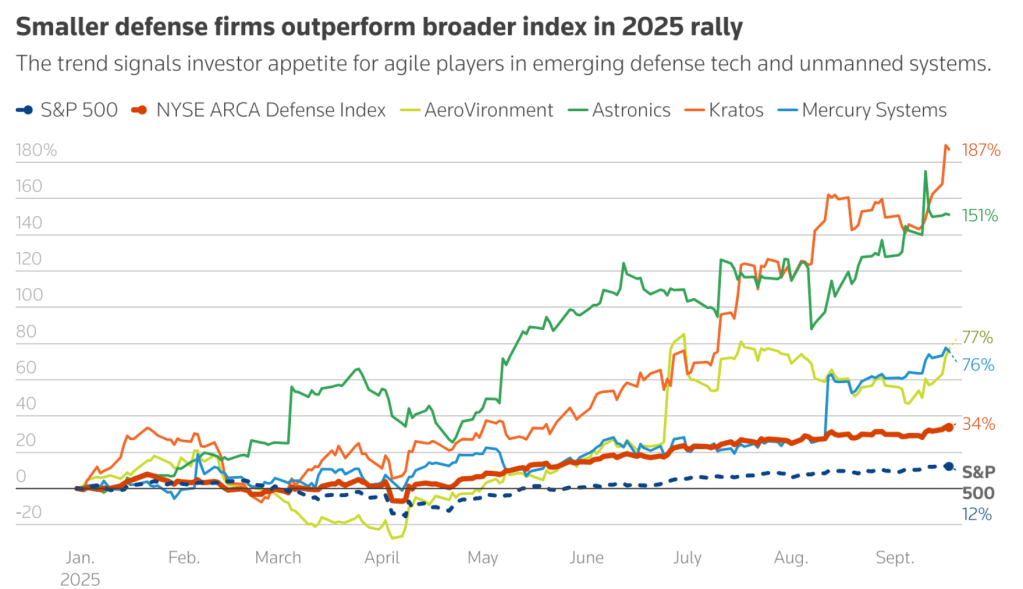

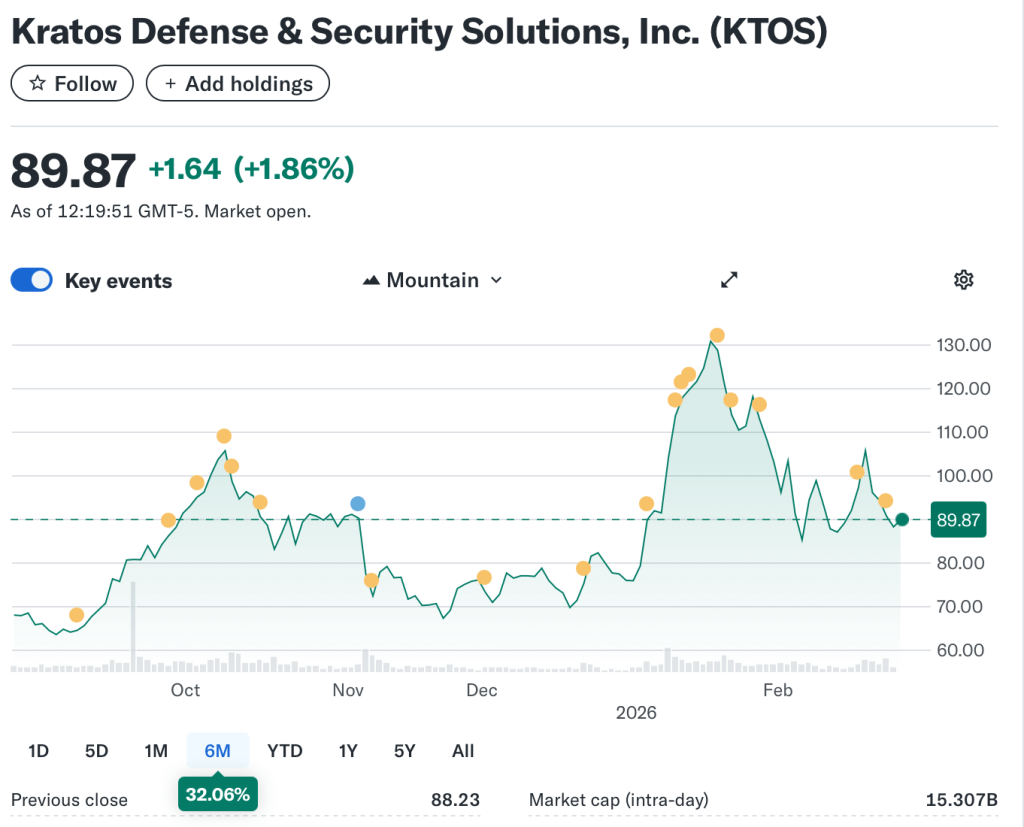

2. Kratos

Kratos Defence and Security Systems is a small/mid-cap US defence company, wwhich specialises in combat drones, hypersonic test infrastructure, and satellite electronics. It is positioned for affordable, high-performance mass systems.

The company has an attractive product portfolio, one of the few publicly traded drone combat enablers. The company published on their website on 26th of February, that they had won a contract worth $12.4 million, in unison with GE Aerospace, ‘to design a next generation engine for small Collaborative Combat Aircraft (CCAs). This is the development of its GEK1500, following the success of the GEK800, this new product has the potential to power unmanned aerial systems, missiles, and CAAs. Further, the WC-58A Valkyrie drone is still in early stages of its development, this will have to be watched to see is this product could be a profit driver. Kratos therefore stands in a great position to capitalise on incumbent demand aforementioned for space applications, with Germany, France, and the UK signalling needs to be met.

In terms of future growth, the caveat is that due to development of the product, the company is trading more symbolic of a venture-style public tech company. The risk is whether they stay experimental, and it doesn’t become a full procurement program. This can be negated by the strong record of contracts with the US Department of Defence (DoD), including the $1.45 billion 5-year contract to advance hypersonic testing, plus $68.3 million for a Hypersonic Materials testing facility. These locked-in repeat contracts are based on testing, equating to lower technical risk failure.

Regarding the most recent company financials for Q4 2025, they had revenue of $345.1 million, beating estimates by roughly 5%. Its operating margin is 2.93% and profit margin of 1.63%, which is low for defence. If you believe their drone capability can scale into large procurement and Kratos becomes, margins have the capability to double, reflective of their ‘unfunded backlog of $1.573 billion, indicating strong future revenue visibility’ according to investing.com. The high forward P/E ratio of 188/68 is also reflective of this. A usual forward P/E ratio for defence is 20-40, BAE systems sitting at 23.75, and Saab sitting at 45.25. The stock is paying for profits that don’t exist yet. The markets are pricing in explosive profit earnings, however, if earnings don’t perform as expected the stock will drop substantially. The beta (5 year) is 1.09, meaning positioned above 1 it moves slightly more volatile (10-15% more) than the market average, but not extreme. Its only 1.09 despite the wild valuation, high P/E ratio as defence spending is relatively stable, and government contracts reduce the cyclicality of these stocks.

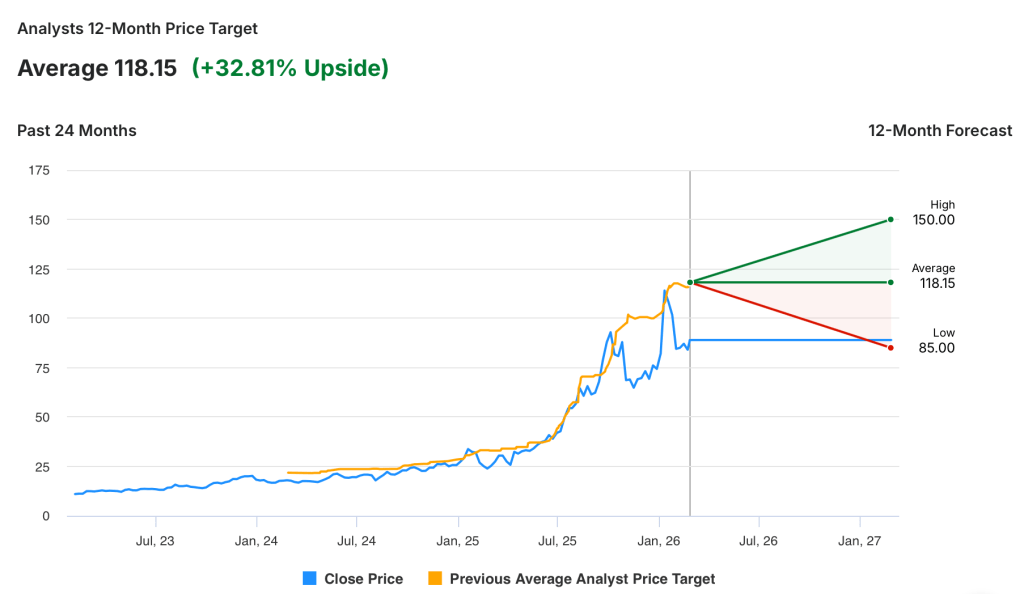

Overall, it’s a good stock to go long on if you believe drones scale into large procurement, margins double, it becomes a core autonomy supplier. It would be considered a less wise choice if growth stagnates at the demo stage, valuation compresses, and it stays as an experimental venture style company. All analysts are proposing a buy, with the average 12-month price target of 118.15, except a few outliers of holds coming from UBS and Piper Sandler, advocating a hold, yet no sells present.

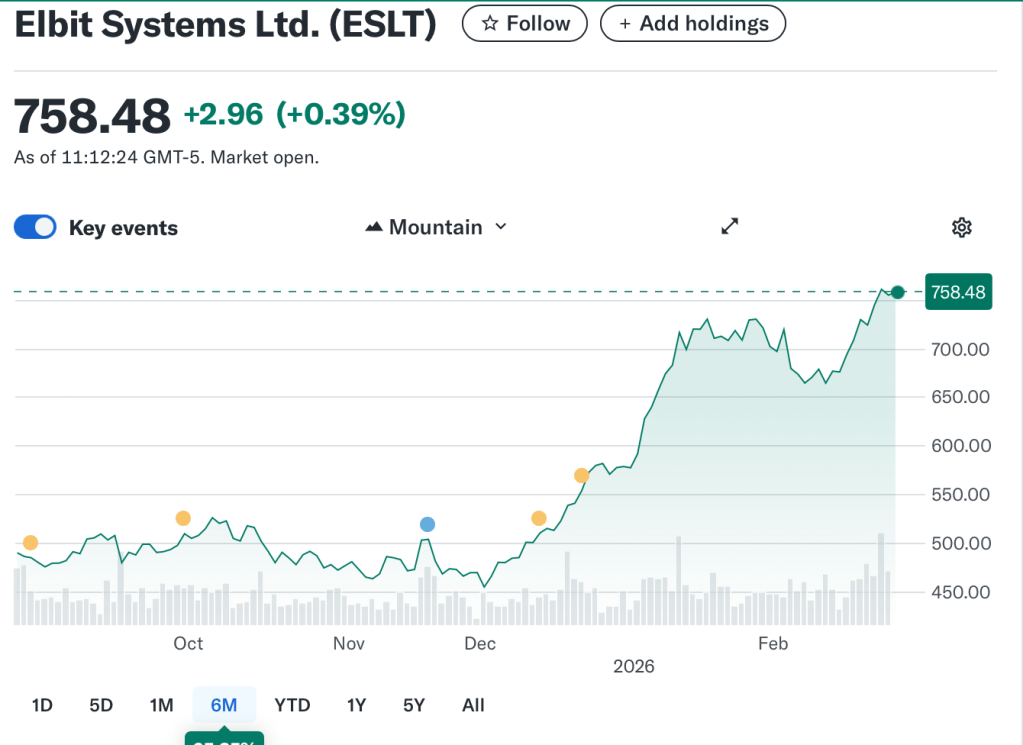

3. Elbit Systems

Elbit Systems is a large cap, Israel-based defence and electronics company, specialising in aerospace, land systems, C4ISR and electronics. Their key products include unmanned aerial vehicles (UAVs), including the Hermes 450, Hermes 900, and Hermes 650 Spark. These UAVs are driving its sales.

The company has a record-high backlog of orders, equalling $25.2 billion which has only been growing, with 69% coming from outside Israel, in Europe suggesting strong revenue visibility. A bounty of fresh contracts has been announced in February, covering $435 million for advanced land systems, $277 million for turrets and munitions, $100 for digital warfare, and $130 million for systems on helicopters, just this month.

The attraction of Elbit Systems is that adverse to Kratos and Rheinmetall, Elbit has a negative beta of -0.2 to -0.4, which is also rare for defence. Therefore, it is a diversifier in risk-off markets, this is attractive for portfolio construction providing a hedge. This can help shield capital if Rheinmetall and Kratos drop. This doesn’t mean this negative beta or Elbit systems is risk-free, if geopolitical risks in the Middle East, especially with Iran, trails into impacting delivery schedules, then this could shrink Elbit Systems’ valuation.

Divulging financials, compared to Rheinmetall and Kratos, the company has better margins, with a net profit margin at 5.91%, an adjusted EBITDA margin 10.5%, an operations margin between 5-8%, and a Gross profit margin 24.0%. Although these figures should be better for a large cap stock, with a market cap of 35 billion USD, especially one that’s defence. A good range for a net profit margin should be between 7-10%, EBITDA margin between 12-18%, operating margin 10-15%. Except for a defence stock, its gross profit margin is fairly good, Rolls Royce gross profit margin is 25.80%.

You could say some of Elbit’s less ample financials, is reflected in its ratings, with a varied mix, but a mostly hold’s ratings suggested, coming from Morgan Stanley and BofA as published by Investing.com, with few buys. There are no active sells.

The sentiment of a hold appears to be the right ethos currently, reflecting on stats like its backlog order and its gross profit margin. If things took a turn into becoming a risk-off environment for defence, then Elbit Systems may be a good option.

Disclaimer: Not financial advice.

Leave a comment