Blue Owl Capital is a leading US asset management firm, founded on the back of a merger in 2020, consisting of Dyal Capital founded in 2010, and Owl Rock Capital Group founded in 2016. Blue Owl specialises in private credit, GP stakes, and real assets, with $307 billion AUM, just about half of these assets sitting within Private credit.

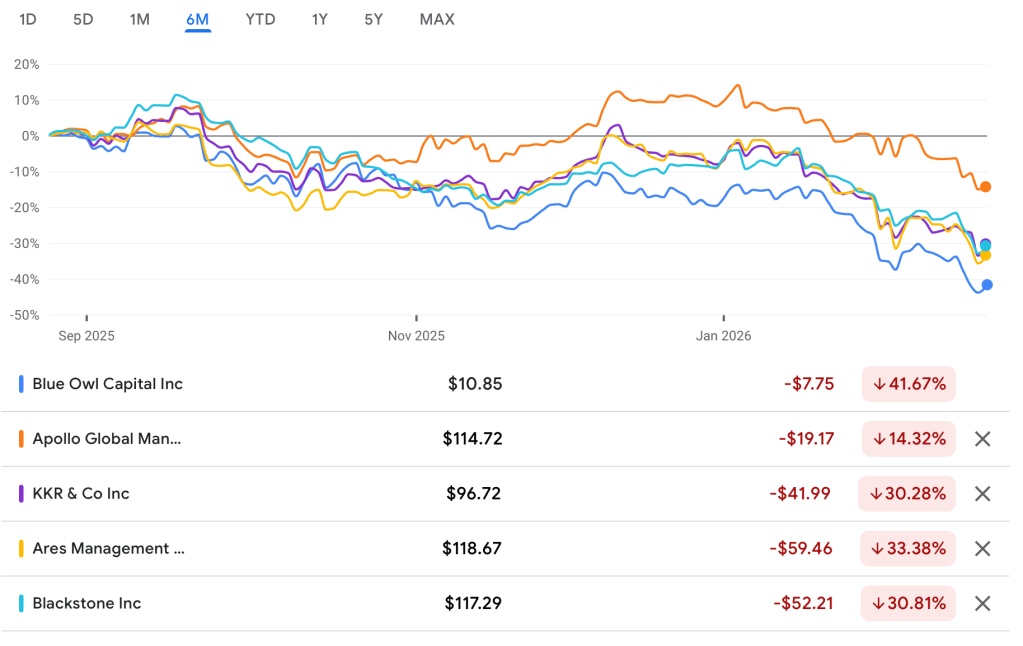

Last week, the company put a stop in place to stop retail investors from exiting, i.e., withdrawing their money from a specific retail-focused private debt fund with a 12% concentration on software assets – OBDC II (Blue Owl Capital Corporation II). Why this matters – foremostly on a fund level, investors prior were able to pull their capital equating to 5% of the fund every 3 months, according to the FT. Secondly, these strong ruminations around this halt, is what it means on an optics level. It signifies something else wider for what CNN Business calls a ‘shadow banking’ industry. The size of the private credit industry was estimated to be $3 trillion at the start of 2025, compared to $2 trillion in 2020 states Morgan Stanley. It has been thought stress has been spreading within it for some time, signified by the major private credit players like Apollo, KKR, Ares and Blackstone all seeing plentiful drops, Ares fairing the worst second to Blue Owl, who is contestably now in light of recent events, in the eye of the private credit storm (shown below).

The FT writes how this bout of doubt stems from not just ‘falling rates and underwriting’, but sequestering capital heavily into software, which has high rates of project failure, rapid obsolescence, and able to be heavily tainted from AI happenings. The fall of Tricolor and First Brands in September 2025, both companies which received private credit are emblematic that this qualm is not just chatter but can easily be substantiated into real losses for banks, such as Barclays which took a £110 million charge. There is serious concern that private credit risk is systemic due to interlink with sell-side banks and insurers with the sufficing of revolving credit facilities. Moreover, not just idiosyncratic risk, as they pronounce themselves to be, based on their bespoke, illiquid, and lock-up structure – and instead, the private credit industry will become a financial locus of contagion.

This redemption standstill is also conjoined with a sell off by Blue Owl of 1.4 billion dollars of assets from three of the BDCs, with $600 million coming from OBDC II.

Nonetheless, the internal financials actually give a strong indication of a healthy company, efinancialcareers.com stated the firm ‘employs circa 1,365 people. Last year it paid them a combined $1.3bn in bonuses plus a further $765m in compensation from “fee related earnings”’. On top of this, the Q4 2025 data which was released on February 5th, shows they beat both top and bottom-line estimates, revenue was $755.6 million exceeding the forecasted $718.37 million, plus adjusted earnings per share up to $0.24, beating $0.23 predictions. These figures for the end of last year may soon be less persuasive of their health. Deutsche bank has downgraded Blue Owl from a buy to hold today, 24th February, along with lowering the price target from $15 to $10 dollars a share. The share price has dropped an alarming -42.36% over the past 6 months. With the company’s Q1 earnings set to be released in May, it will be interesting to see if despite all the changes, if behind the scenes the firm still maintains its financial soundness in the near future.

Disclaimer: not financial advice

Leave a comment