The Office for National Statistics (ONS) reported today that the UK inflation has fallen to 3% for January, down from 3.4% in December.

The ONS believes this surge was caused by the cheaper cost of motor fuels and airfares, as well as a stabilising cost of meat prices.

UK overall unemployment has risen to 5.2%, the highest level in five years. This is coupled with youth unemployment rising too to 16.1% for 16–24-year-olds, also the highest level since 2015. The youth rate now stands higher than the EU’s, the first time in history since records began in 2000.

Why this youth unemployment number is a focal point, is that it is seen as diagnostic for an economy, as it is highly sensitive to business confidence and also very cyclical.

These two figures of unemployment and inflation are shifting the focus for the UK economy away from inflation risk to growth risk.

Overall market consequences following these two indicators:

- Rates likely down.

- Good for bonds.

- Mixed for equities.

- Slightly negative for the pound.

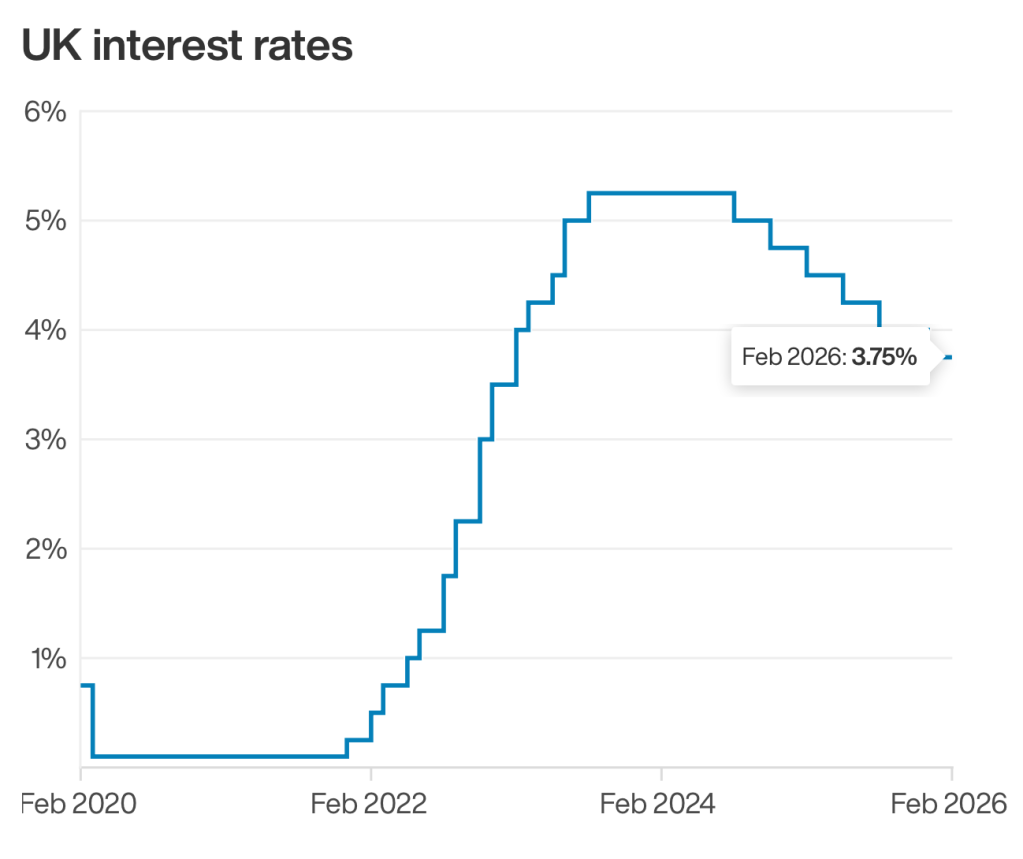

– Interest Rates

Inflation dropping, now gives a clearer path for a rate cut to be imminent in March; an 80% chance recorded by money markets according to The Guardian, based on swaps contracts. The original consensus forecasted a rates cut, with a mixed bet between the timing of either March and April. The pessimism that April may still could happen instead, is due to the underlying pressure of services inflation. The FT reported services inflation is still looking sticky as it fell only 0.1%, to 4.4% from 4.5%.

Unemployment being higher than expected gives an addition to this strengthening case for a cut at the March meeting. As youth unemployment signals business confidence, and overall unemployment gives an indicator of UK consumer confidence, and disposable income’s of working adults.

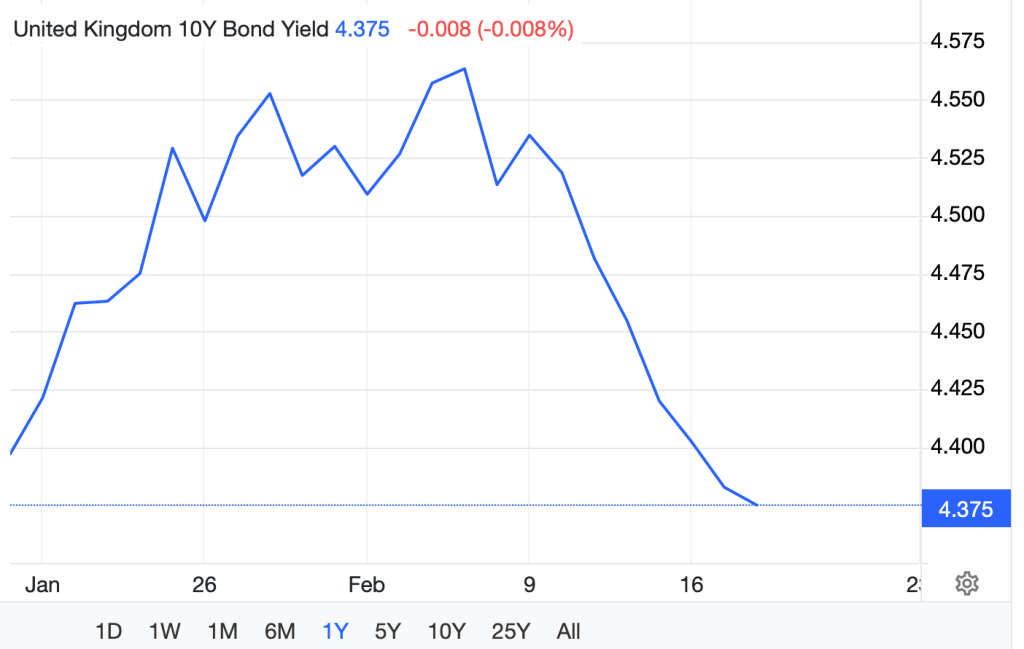

– Gilts

When inflation is low, it is usually positive for UK government bonds (gilts). This is due to the tie inflation has to interest rates, which in turn impacts bonds.

Gilts fell slightly in reaction, with the 10-year gilt yields going down to 4.37%, the lowest since January 14th as observed by Tradingeconomics.com.

When interest rates come down, and inflation also comes down, lower short-term gilt yields would be priced in, with a steepening yield curve. Long-term gilt yields should observe less of a reaction.

This is because gilts pay fixed interest (coupon) payments. When inflation falls the real value of those fixed payments rises. This means gilts become attractive, so investors are willing to pay more for gilts. Therefore, prices rise, and yields fall. In effect, lower inflation makes gilts more desirable as it means any money invested, retains more purchasing power.

This idea is embedded by a projection from Bloomberg which quotes that ‘UK bonds will rally in 2026…driven by Bank of England interest-rate cuts.’

Increasing unemployment, generally aids as a catalyst for falling bond yields, (again, most prominently in the short-term). This is due to the link the unemployment rate has on interest rates, as discussed previously. As alluded to, high unemployment signals slower economic growth, which a cut in interest rates can aid in improving.

– Equities

Equities see a tug of war between improved margins and potential revenue declines, when based on inflation and unemployment data.

Lowering inflation can act as a tailwind, as it should act as a boost for consumer confidence due to more disposable income. Lowering inflation on the other hand, can also be a mitigator to equity gains, if instead its consequence shows instead in the form of weakened consumer demand, and diminished corporate returns.

The impact unemployment data on equities also has a nuanced result. In the short-term, usually markets observe counter-intuitive rallies, via the interest rate channel. Since unemployment signals future rate cuts, and accordingly easier access to cheaper funding for companies and improved earnings, which shows up in the stock prices. However, in the earnings channel, this could dampen stock prices as companies should theoretically struggle, as they will be sitting within a weaker overall economy, meaning less consumer spending. Therefore, justifying the declaration of a ‘mixed result.’

In the short term, the equities market has currently priced in a boost. The FTSE 100 closed at 10,686.18, up 1.23%, reaching a session peak on the 18th February of 10,715.77, as stated by Yahoo Finance UK.

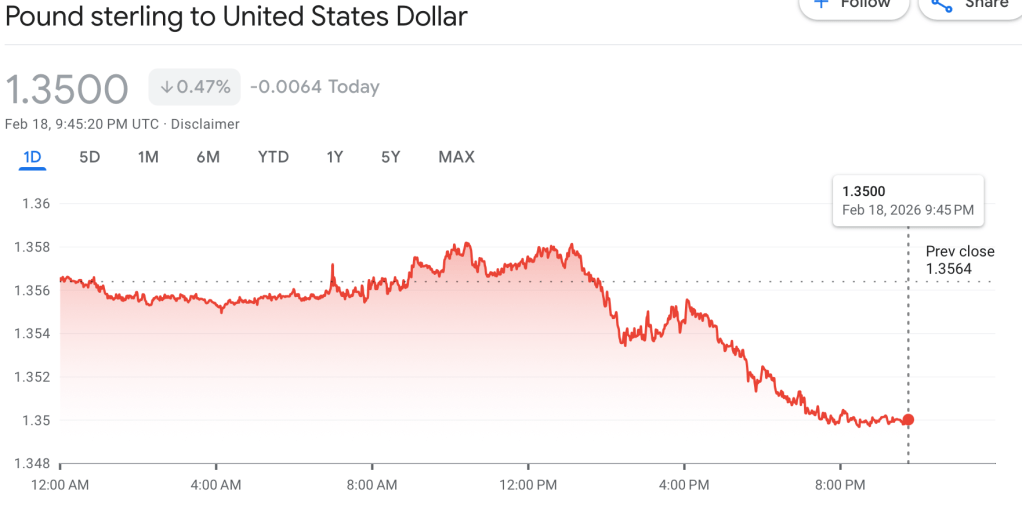

– Sterling

In the immediate aftermath of the announcement of the inflation and unemployment data, Reuters reports sterling has stayed steady against the dollar in the 1.3500-1.3600 range.

For currency traders, a bigger ensuing situation that will be adhered to, is the growing political situation with the UK Primer Minister.

However, over the long-term this could look slightly different. Inflation and unemployment figures could become stronger headwinds, causing sterling to weaken. This is due to the reduced rates prediction, accordingly a reduced yield for holding British assets.

Increasing UK unemployment, which is at a much higher rate than within the past decade, can push foreign investors away from the UK. They would instead be drawn to nations with stronger growth and economic stability, again weakening the pound and its attractiveness.

Leave a comment