What are Options?

Options are a type of financial instrument called a derivative. They derive their value from an underlying asset, such as stocks (e.g. a single stock such as TSLA – Tesla), a stock market index (e.g. NDX, the NASDAQ-100), or exchange-traded fund (SPY – S&P 500 ETF).

An option is crucially a contract; a buyer pays a premium (essentially an up-front fee) to purchase this contract, which gives the buyer a right, but not the obligation to exercise the option. The buyer is not forced in the future to sell or buy an option up until the specified expiration date, as it’s not an obligation. Much like car insurance, where you pay an upfront premium for the future right to exercise a payout if needed, but you may never use this ability to claim outright.

A call option allows the buyer the right to exercise and buy the asset at its strike price up until the contract finishes. A put option stands in dichotomy, with the difference being the right to sell, instead of buy. Call buyers benefit from rising prices; put buyers benefit from falling prices.

Much like a car insurance contract, an options contract loses intrinsic value up until the end of the expiration date, as the buyer of an insurance, the payoff of investing in the insurance has not been utilised. This can be seen as time decay; this decay compounds and speeds up in the very few weeks right before the end.

A basic definition of options allows for understanding how option Greeks work. The Greeks are ways of understanding how an options price is sensitive to changes in different market conditions, and how they affect an options position (i.e. ITM, ATM, OTM). The Greeks are essentially like dashboard warning lights, if a dashboard light comes on, it is less reflective of the symbol seen, and wholly reflective of the underlying change, in this case, a car engine, that would be the option in this example.

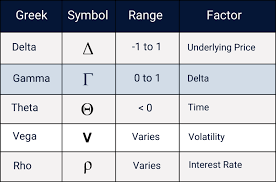

The Five Main Greek Options: Delta, Gamma, Theta, Vega, and Rho.

1.Delta Δ – Directional Risk

Delta is the most commonly known Greek option, and measures how much an option’s price changes for a $1 move in the underlying asset. Delta acts as a directional indicator and probability estimate, ranging from -1 to +1, and looks different for a put option and a call option.

Delta matters as a measurement tool, as it indicates directional exposure and can be used for delta hedging. Moreover, delta can approximate the probability of an option expiring ITM.

Call option: Delta range is from 0 to +1.

Put option: Delta ranges from 0 to -1.

For example, a call option with a delta of 0.60, if the stock rises $1.

2. Gamma (Γ) – Delta’s Sensitivity

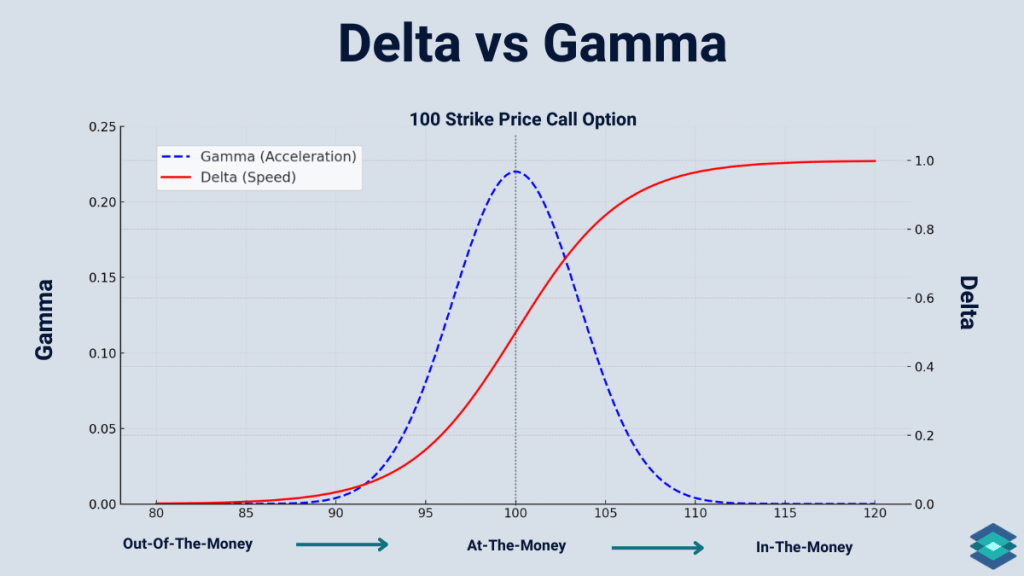

In trading, gamma is connected to the first Greek option delta, and measures the rate at which an option’s delta changes as the underlying asset moves $1, i.e. indicates how quickly delta will shift. Think of gamma as the delta of the delta.

A high gamma measure indicates that delta could change dramatically with even a small price change. Gamma is highest for ATM, and correspondingly decreases for ITM, and then is at its lowest for OTM. Gamma is used to assess the risk of delta changing.

A high gamma = delta is changing dramatically, with small price moves, and ITM.

A medium gamma = mid-level movement, but more than low gamma, signalling stability, and ATM.

A low gamma = delta is changing slowly, indicating more stability, and less risk from rapid price swings, and OTM.

In other words, delta tells speed, gamma measures relative acceleration.

3. Theta Θ – time decay

Theta is the Greek that measures an option’s sensitivity to the passage of time, holding all else constant. All else constant means any other changes, such as volatility and interest rates, remain static.

In effect, theta represents the rate at which time decay has on the value of an option.

Theta is worked out by dividing the option value by the time (days or years).

Negative theta infers that the option loses value over time; this is the case for most vanilla options, along with both call and put options.

A positive theta means the option’s value augments upwards over time, this can happen for certain exotic structures and/or are in ITM puts.

The maximum level of time decay happens for ATM options. Theta magnitude is small when an option is deep in ITM and deep OTM. Theta is not constant; it increases in magnitude as expiration nears.

Theta is more negative for options at OTM and ITM, as these situations infer high volatility and a higher option premium. Accordingly, it has been exhibited that Theta is not constant; it increases in magnitude as expiration approaches. A small daily theta pertains to a long-dated options, and a large daily theta is related to short dated options.

4. Vega – Volatility

Vega is the amount an options price will change, its sensitivity, to a 1% change in the underlying assets’ implied volatility, holding all factors constant.

Vega is calculated by dividing the option value by the volatility of the underlying asset.

High Vega = occurs when options are ATM and have a long time till expiration, this can be due to there being more time given for price fluctuations, which produces uncertainty. High Vega infers an option has the most extrinsic value, and therefore the most sensitive to changes in implied volatility, reflecting market uncertainty. Most long call and long put options have a positive Vega.

Low Vega = Vega decreases as options get closer to expiring or move further into ITM or OTM. Most short options have negative Vega.

Vega is an important indicator as it represents the level of uncertainty and is an important tool to capitalise on in volatile markets. This is due to Vega being able to capture changes in market sentiment, even when the underlying asset’s price remains stable.

5. Rho ρ – Interest rate

Rho is arguably the least used and least important of the Greek options. It is a measure of how the price of an option’s price changes in response to changes with a 1% change in the risk-free interest rate (the interest rate paid on US treasury bills. Rho is typically expressed as a dollar amount. Interest rates have an impact on an option’s value, as they impact the cost of carrying the position over time.

Rho reflects the sensitivity of calls and puts to rate changes. Calls typically gain in value as rates rise, while puts often lose value. Rho is less important.

High Rho = Options with a longer time to expiration have a higher rho, and accordingly are more sensitive to interest rate changes. Call options and long options generally have a positive rho.

Low Rho = Rho is negative for long puts and short calls. This is because higher interest rates decrease put premiums. High interest rate environments mean a long put is less favourable.

Leave a comment