Derivatives are financial contracts where the value is derived from an underlying asset, such as a stock, bond, interest rate, commodity, or index. Derivatives are used to manage risk through hedging, speculate on the underlying price movements, or trade with leverage, without having to buy the asset itself. Derivatives come in the form of options and futures. Other forms of a derivative can also exist in the form of spread betting or contract for difference (CFD) trading, which speculate on the price movements of a derivative; these latter two types still constitute as derivatives, as they track the price of an underlying asset.

Derivatives can be seen from 3 different lenses.

- Rights vs. Obligated based:

Rights-based derivatives

Rights-based deirvatives give the holder the right but not the obligation to buy or sell an asset; options fall into this category.

A key feature of rights-based derivatives is that the holder, once they pay a premium and possess the contract, controls the right on whether to exercise. The rights lay in the holder’s control. The seller (also called the writer) who essentially sold the contract, has an obligation to fulfil the contract at the holder’s request. The pay-off of a rights-based derivative is asymmetric; moreover, the Greeks apply here.

Hedgers would use rights-based derivatives, as this type of derivative can be used to protect against adverse price movements, keep upside potential, and pay a premium as a form of insurance. A hedger would use a rights-based derivative to reduce risk, not necessarily as a profit-maximising tool.

Alternatively, a speculator would see a rights-based derivative as a bet on direction and volatility, limiting downside risk and offering high leverage. A trader would purchase a call option expecting a sustained upward trend in the stock price.

Obligation-based derivatives

Obligation based on the other hand, is where the buyer and seller both have an obligation to conduct a transaction at a future date. This can be forwards, futures, or swaps. At maturity, both parties have no choice but to fulfil the terms of the contract. An obligation-based derivative typically has no upfront premium, except for margin (this collateral, however, is not necessarily a cost).

An obligation-based derivative pay-off looks slightly different, as it has a symmetric payoff; there is unlimited profit and loss potential. One party’s gain is one party’s loss. However, the Greeks do not apply here.

In other words, what could be seen as what determines whether a derivative is considered rights or obligation based is based on the condition of the holder (the buyer) of the contract, as the deciding factor.

Hedgers can use obligation-based derivatives to lock in prices to ensure certainty, eliminating both upside and downside risk. For example, a client who is an airline, may use fuel futures to lock in fuel costs to avoid future price uncertainty.

Alternatively, a speculator would use an obligation-based derivative to make a strong directional position, ensuring no premium risk, with a high risk, high reward. For example, a trader purchasing an index future may be under the guise of the market to rising.

2. Linear vs. Non-Linear

Derivatives categorised under this lens are distinguished via their payoff structure. Payoff is the profit or loss of a derivative from the contract.

Linear Derivatives

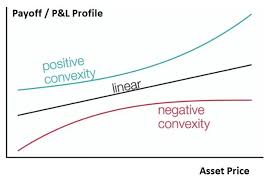

Linear derivatives have a pay-off structure that changes proportionally, i.e., one-to-one with the price of the underlying asset. A 1-unit change in the underlying asset causes a 1-unit change in the derivative value. Therefore, payoff is symmetric; equal upside and equal downside, but the gains and losses are unlimited.

Linear derivatives are forwards, futures, and swaps, they have little convexity; the Greeks do not apply.

Linear derivatives are used by hedgers to lock in prices or rates and remove uncertainty from future cash flows. Speculators see linear derivatives as a way to gain high leverage, and arbitrageurs use them to exploit price mispricing, ensuring price alignment between spot and derivative markets, which in turn can accumulate low-risk profits.

Those aiming for arbitrage can use linear derivatives to exploit mismatches between spot and derivative markets.

Non-Linear Derivatives

Conversely, non-linear derivatives have a payoff that is non-proportional to the underlying asset price. These refer to instruments which involve optionality and volatility, e.g. a call option.

Non-linear derivatives provide an asymmetric risk-return; losses are often limited for the buyer. Common examples include call and put options, plus exotic options (barrier, digital, Asian)

This means that the asset’s price, and its sensitivity (the delta) changes with price, time, and volatility. The pay-off when graphed is convex or concave, rather than a straight line seen for linear derivatives.

Non-linear derivatives are used by hedgers to obtain downside protection whilst retaining upside potential, by speculators to benefit from leverage and volatility-based strategies, and by institutions to create bespoke structured products.

3. Exchange-traded vs. Over-The-Counter:

The third, and most popular, lens on which to see derivatives and how to separate them, is based on the location derivatives are traded, i.e., on or off a market. The derivatives market is not a single physical place, but rather a point where buyers and sellers meet to partake in an exchange. This can be on a listed exchange, such as the CME (Chicago Mercantile Exchange) or ICE (International Exchange).

Exchange Traded Derivatives (ETDs)

ETDs are standardised derivative contracts traded on organised exchanges, such as those like the CME or ICE. They are cleared through a central clearing house in order to lower default risk. Since ETDs are standardised financial contracts, they have set out details such as the size, maturity, and strike price. For example, ETDs can be futures, commodity derivatives, or vanilla options.

The main benefit of ETDs over OTC derivatives is the high-level standardisation and regulation, this consequently results in low counterparty risk, this results in the products offering a higher level of transparency and liquidity. For corporations these can be beneficial for more tailored risk management. For institutions when increased complex and large transactions are conducted, ETDs are suitable.

Over-the-Counter Derivatives (OTC Derivatives)

Opposingly, OTC derivatives happen off an exchange. They essentially happen on a private market, as these are privately negotiated bilateral agreements, traded directly between two parties. There is no presence of a central exchange. This results in high counterparty risk and less transparency. The customised nature results in higher flexibility, meaning exact hedging is possible.

OTC derivatives offer less liquidity, with only light regulation. These derivatives are still overseen by collateral regulation. Examples of OTC derivatives include forwards, swaps, and exotic options.

Leave a comment